Beyond Adyen and Stripe: Unlocking True Payment Optimization with POPs

Author: Steve Glover, Payments Lead

The IDC MarketScape Vendor assessments for Online Payment Platforms and Omni-Channel Payment Platforms were released a couple of weeks ago. Stripe was judged the best Online provider, closely followed by PayPal (Braintree) and Adyen. For Omni-Channel, Adyen was crowned the winner.

Modern payment platforms such as Adyen, Stripe and Nuvei have some top customers all around the world and continue to grow rapidly. These facts reinforce that they have good products, certainly when compared to legacy providers.

And yes, merchants get omni-channel capability via a single unified platform (even with Stripe though they weren’t included in that category), they get access to a wide range of traditional, local, and alternative payment methods, they’re much more developer-friendly, there’s a decent built-in fraud screening tool, self-serve reporting, local acquiring for international merchants, plug-ins to major commerce platforms, etc.

But All Is Not As It Seems..

However, I also hear quite a lot of negative feedback from merchants aimed at the modern players that win all the awards.

Although Adyen and Stripe are very well-respected in the industry, modern payment providers are not always the panacea some merchants believe them to be. Without singling out any one provider, I know many merchants who aren’t happy with support when things go wrong. They’ve had outages, blame games when issues arise, authorization rates not where they should be, limited flexibility on commercials, often with minimum volume commitments, mixed messages on compliance, cash securities required, merchants being switched off without notice or recourse, and the rules-based fraud tool is a little too manual and cumbersome for some to manage.

Even though their reporting is worlds apart from some legacy players, they were still slow to convert their data into useful dashboards until more recently. Beforehand, merchants had to download and mash together multiple reports to see certain key metrics along the payments lifecycle.

Then there are other issues like not being able to do PIN debit routing in the US, which would rule them out of a lot more deals if more merchants knew about the cost-benefits. And they are expensive, with Adyen targeting net margins of 55% last time I checked. For info, the average large retailer makes ~2-4%.

So why are merchants flocking to Adyen? First, they are really good at marketing. Second, they have a fairly slick group of young, tech-savvy salespeople. Third, and I think increasingly more relevant, is that nobody gets fired for choosing Adyen, in the same way that people used to say “nobody gets fired for choosing IBM” 20-30 years ago!

OK, if you are a merchant and you’re with Worldpay, Barclaycard, or Worldline, then let’s say you’re at 50% on the hypothetical scale from really poor performance (0%) to completely optimized (100%). Moving to Adyen or Stripe may get you to 80% and feel like a game-changer. Increased time-to-market, more features out of the box, less technical debt, more agency over performance due to the online self-serve tools ad customizations, your acceptance rates have gone up a bit, and all of this is worth the additional cost you now pay.

True Optimization Requires a Different Approach

At Bankhawk, we see more and more global merchants now actively plotting how to get closer to 100%. To do that, you really need to use multiple gateways, multiple acquirers, at least one dedicated fraud tool, efficiently manage FX and multi-currency pricing, and be able to access local payment methods, which often require local entities or are not available with Adyen and others. This needs to be combined with robust internal processes around product, UX, fraud, BI, etc.

Of course, this approach can carry massive internal and external investment and it needs a fair amount of knowledge and expertise to set up and maintain, which is the reason why many just choose Adyen. But a new breed of payments companies, payment orchestration platforms (POPs), are now gaining traction. Companies such as Apexx, Spreedly, Gr4vy, Cellpoint Digital, Fabrick, and Primer.

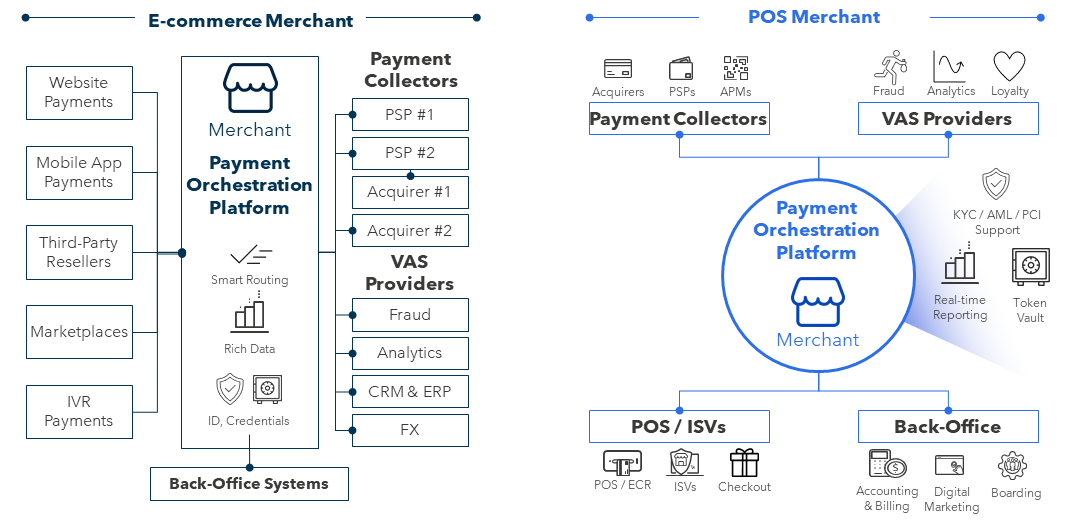

They are acquirer-agnostic and offer one-click access to hundreds of payment providers (including the likes of Adyen and Stripe), fraud providers, and payment methods globally, cascading rules to optimize approval rates and recover failed transactions, increased redundancy (kind of), smart routing to the lowest cost processor or network, and more, all via a single integration. Much of this can be configured without any code, and reporting and reconciliation from multiple providers are transposed into a single source of truth. See image below for a high-level view of the typical architecture.

Source: Flagship Advisory Partners

This all begs the question of how to choose a POP for your business. The marginal gain versus an Adyen or Stripe will be very merchant-specific and, while ROI calculators are available online from many of the names above, the results can be wildly different, suggesting that there’s a lot of guesswork until you actually go-live (I do appreciate that they are clearly only intended to be indicative).

Where to Start (and Finish)

So how do you know whether it will be worth it for your business? How do you quantify the upside? Which POP is best for your industry and use cases? What do you do if you’ve recently integrated Adyen or Stripe? And how do you craft a business case to convince internal stakeholders that this project needs to happen over all the others?

These are all questions worth considering if you’re looking to take your payments performance to the next level. To do this requires a strong understanding of business performance and total cost of ownership of the existing solution. For, example, what’s your web conversion rate? How are you using 3DS and what is the drop-off rate per country or issuer or BIN. How do your fraud and chargeback rates compare to peers? How many transactions are you blocking due to suspected (not just actual) fraud? What’s the bank authorisation rate? Can you easily analyse decline reason codes and what is your strategy to recover failed transactions, if there is one?

Then, operationally, do you want to ship to new markets or offer new payment methods but the cost is too great? Can you easily A/B test different checkout parameters? Are you able to spot refund or other policy abuse?

The list of questions is endless but thinking about them helps to visualise the theoretical upside from moving from 50% to 80% towards 100% on the “payments efficiency scale”. Most enterprise businesses can deliver millions to top- and bottom-lines if they know where to look. Some of this can be delivered with legacy and more modern payments providers, but I think POPs will continue to be an invaluable tool to get merchants firing on all cylinders and closer to 100%.